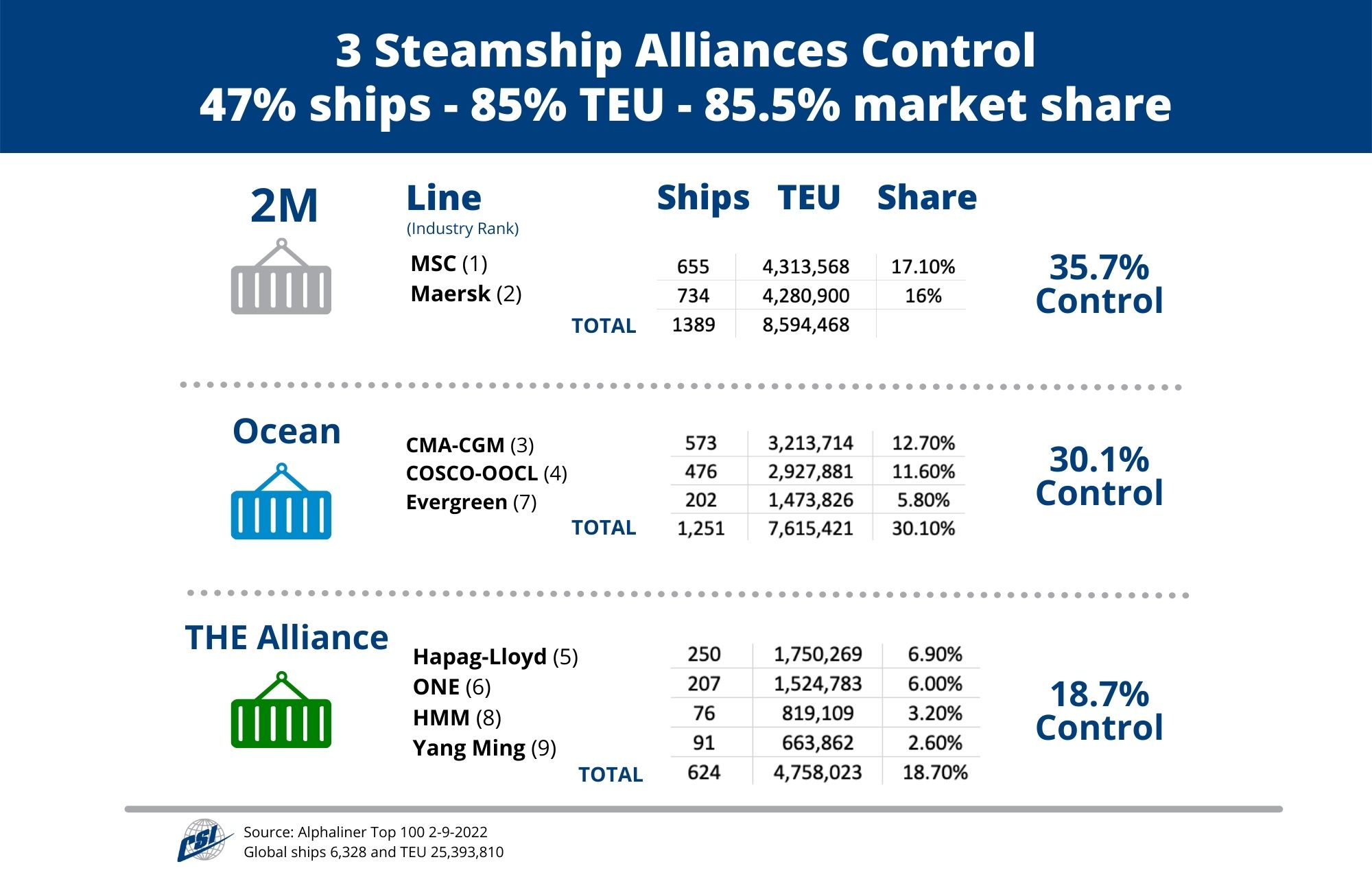

In 2017, three major shipping Alliances formed. Over the last several years, they have taken control of space and rates. Alliances allow the carriers to share space and container volumes through vessel sharing agreements within the alliance. This graphic shows the control of ships, TEU and market.

This structure gives carriers control of pricing by sharing the cost of pulling (blanking) vessels out of service within the alliance to match capacity with container demand. Operating within a network the carriers can adjust capacity quickly, keeping space tight and rates steady.

This structure gives carriers control of pricing by sharing the cost of pulling (blanking) vessels out of service within the alliance to match capacity with container demand. Operating within a network the carriers can adjust capacity quickly, keeping space tight and rates steady.

When container volumes start to increase, carriers can be slow in returning vessels into the system. By delaying deployment of parked vessels, they drive up demand for space, allowing them to increase spot market rates.

For importers, it’s a good idea to diversify your international supply chain as much as possible. Working with a quality forwarder with competitive steamship line contracts across the alliances helps to balance both service and pricing risk to value and benefit from changing market conditions.